Language | Operations | Organisation | Process | Strategy

STAY CONNECTED AND SIGNUP TO RECEIVE INSIGHT updates

Who wouldn’t want more for less? More profit from less investment? More government services for fewer taxes? More charity work for less administrative overhead? But what measures will help us hit or exceed our productivity ambitions?

This is part 1 in a series. Read the other part here: Managing accounting’s relevance

[ Listen to the audio version, read by David Hodes]

The organisations we work in, manage and lead are complex systems that have a standardised way of measuring what is happening with the enterprise as a whole. We all know about the balance sheet, profit and loss, and cash flow statements. But, when measuring what goes on within the organisation, things get much more complicated and less standardised.

We seem wedded to the idea that because our enterprises are so complex, whether big or small, we need to break them up into functional areas to manage them effectively. Thus, we have Sales & Marketing, Operations, R&D, IT, Finance, HR and on and on. And for each of these functions, we design measures that seek to optimise that function’s production.

But will a function measured on what’s optimal for itself actually deliver what’s best for the business? How can we design a measurement system that has the people at the lowest level, those on the proverbial shop floor, measured in such a way that they are empowered to make decisions which they know will be in the organisation’s best interests? How do we get alignment from top to bottom and bottom to top?

“Will a function measured on what’s optimal for itself actually deliver what’s best for the business?”

For now, let’s stick with for-profit businesses, as the lessons readily translate to government and NGO environments. The goal of a for-profit organisation is to maximise return on shareholder funds—or at the very least to provide a competitive return against other businesses in that sector. And before you jump on the ESG bandwagon, social licence is not a goal but rather a necessary condition that must be fulfilled to achieve the goal.

If our goal is to maximise return on investment, what should we measure to determine whether we’re getting closer to achieving it? Here are six critical financial performance questions for which our measures must provide an answer:

1.Is the overall business profitable?

2.Is a given strategic business unit within the overall business profitable?

3.Is a given product or service attractive for us to make and sell?

4.Is a given customer or customer segment attractive for us to do business with?

5.Should we make the product or service ourselves or buy it from a third party?

6.Should we make a given investment?

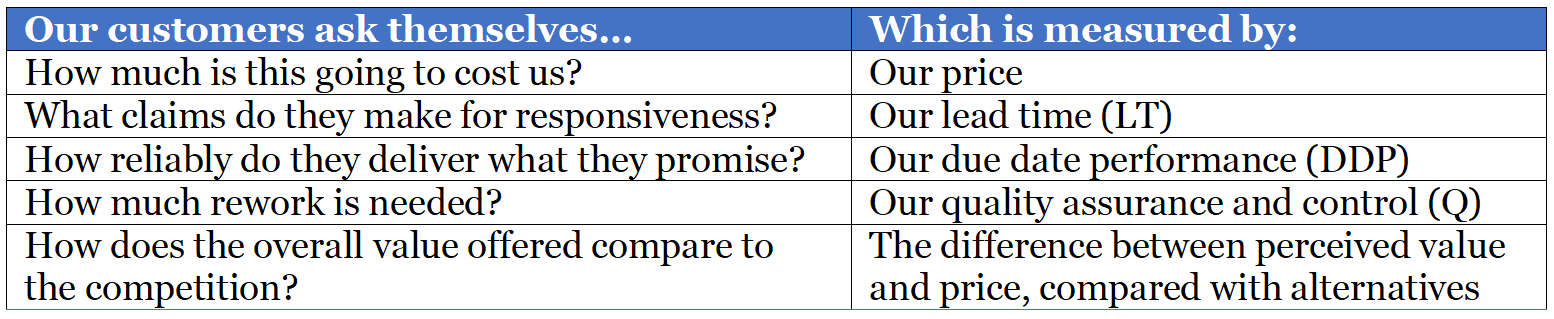

These big questions look inwards at our own enterprise. But we should also consider how our customers will judge our products and services:

And, of course, since we are part of a value chain, we’re asking ourselves the same questions about our own suppliers’ products and services. What will it cost us? How easy is this supplier to work with? And what are the risks? All based on the same measures of their price, lead time, due date performance, quality, and overall value.

The problem with the cost-world paradigm

As already mentioned, at the top level of the organisation, there is a set of measures prepared by the financial accountants that comply with generally accepted accounting principles, such as the balance sheet, profit and loss and cash flow. At the strategic business unit level, it often gets a lot trickier. The relationships, for example, between the producing division and the sales and marketing division are not necessarily at arm’s length. Through transfer pricing, many organisations dictate and often distort the profitability of their business units. Costs are allocated for shared overhead, often in ways that make little sense other than to those who do the allocating. Way down at the shop floor, the measures are often predicated on efficient use of resources to ensure maximal utilisation.

The trouble is that if the measures are set up in this polarising way between different levels of the organisation, it becomes tough to make day-to-day decisions that translate the impact that local actions have on the goal. We need something better to help us become more proactive everyday decision-makers.

Let’s take a closer look at the cost-world paradigm and how it attempts to address complexity by adopting a reductionist approach.

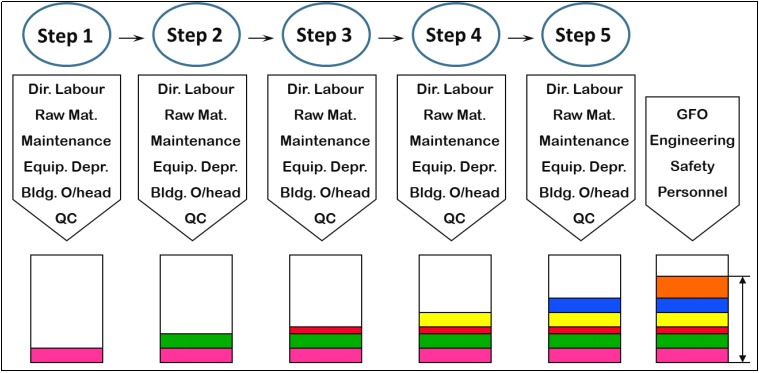

The diagram below shows how a typical product (or service) costing is calculated based on activity—hence, it is called activity-based costing. We start with step 1. The number of labour minutes is budgeted and costed. The cost of raw materials is added for that activity, along with various overhead ‘burdens’ according to a formula calculated by the cost accountants, usually predicated on the proportion of the labour minutes associated with that step relative to the total labour minutes of the combined overhead.

As each step is undertaken, the product (or service) absorbs more and more costs based on direct labour minutes for the activity and their associated absorbed costs until you have a finished product. You can add general factory overheads (GFO) and other overheads such as engineering, safety and assorted personnel at this stage. Looking closely, you’ll find the kitchen sink absorbed into the product costs.

What’s the problem, then, with this method of measurement? Goldratt famously said, ‘Tell me how you measure me, and I will tell you how I will behave. If you measure me in an illogical way… do not complain about illogical behaviour.’

The behaviour induced by such a system encourages managers to produce as much as possible to reduce unit costs. How does this work? The volumes to be made are based on a budgeted number. The allocation of the overhead burden is also based on a budgeted number. Then, by the rules of activity-based costing, if the number of units produced is above what was budgeted, each unit will absorb less of the overhead burden than initially budgeted as more units are passing through in a given period to do the ‘work’ of recovering the costs. The management accountants call this an over-recovery. An over-recovery is credited to the profit side of the ledger, and everyone feels good about the benefit of being more productive than budgeted…until you have piles of inventory and work in process that no one wants to buy.

More egregiously, this costing system pays no heed to the existence of the constraint. No less an authority than the late Charles Horngren, Professor of Accounting at Stanford University, declared: ‘Relevant information is the predicted future costs and revenues that will differ among alternative actions. The existence of a limiting factor changes the basic assumptions underlying the cost and revenue opportunity of a particular action.’ In simpler terms, he wrote: ‘A company will profit maximise when it sells the product or service with the highest contribution per unit of the scarce resource.’

The limiting factor or scarce resource Horngren refers to is the constraint. However, despite the good professor’s advice, most finance departments completely ignore the identification of the scarce resource, often arguing that it is the job of Operations to determine where the bottlenecks are and deal with them. For the most part, Finance and its armies of cost accountants focus on cost drivers, not constraints.

You have to pity Operations as they scour the horizon for greater and greater local efficiencies. In all likelihood, they know where the bottlenecks are, as they need only look for the build-up of work in progress. Bottlenecks, after all, cause logjams. But we all know that accountants set the rules of how the game is played with their activity-based absorption costing. Thus, Operations must be satisfied with scratching their heads in wonder at what happened to common sense and how common practice got to be so out of kilter with it.

How can we make better business decisions?

I’ve mentioned the key measures we need to make better decisions. In my next article, I’ll show how they lead to the throughput-world paradigm for management accounting, which is much better suited to addressing the six questions for financial performance than activity-based absorption costing. After all, none other than W Edwards Deming said, ‘The object of any component is to contribute its best to the system, not to maximise its production…some components may operate at a loss themselves to optimise the whole system.’

Here are the six questions again so you can consider your organisation’s way of addressing them.

1.Is the overall business profitable?

2.Is a given strategic business unit within the overall business profitable?

3.Is a given product or service attractive for us to make and sell?

4.Is a given customer segment attractive for us to do business with?

5.Should we make the product or service ourselves or buy it from a third party?

6.Should we make a given investment?

Are you currently in the cost-world or throughput-world paradigm?

Read Part Two: Managing accounting’s relevance

____________________________

What’s next?

The change to using Theory of Constraints (TOC) as an underlying operating system is both profound and exhilarating. We’ve developed the Systems Thinker Course to bring the ideas into your organisation.

- View the Systems Thinker Course Guide (no email required to download)

- Join us for the Systems Thinker Foundations Workshop (we run this FREE workshop once each month)

- To find out more about these, or any of our services, simply schedule a call

____________________________ [Background image: Stock market or forex trading graph on Shutterstock]

[Background image: Stock market or forex trading graph on Shutterstock]

____________________________